Dusan Petkovic // Shutterstock

The end of card-funded ad spend: Why Meta and Google want businesses off credit cards

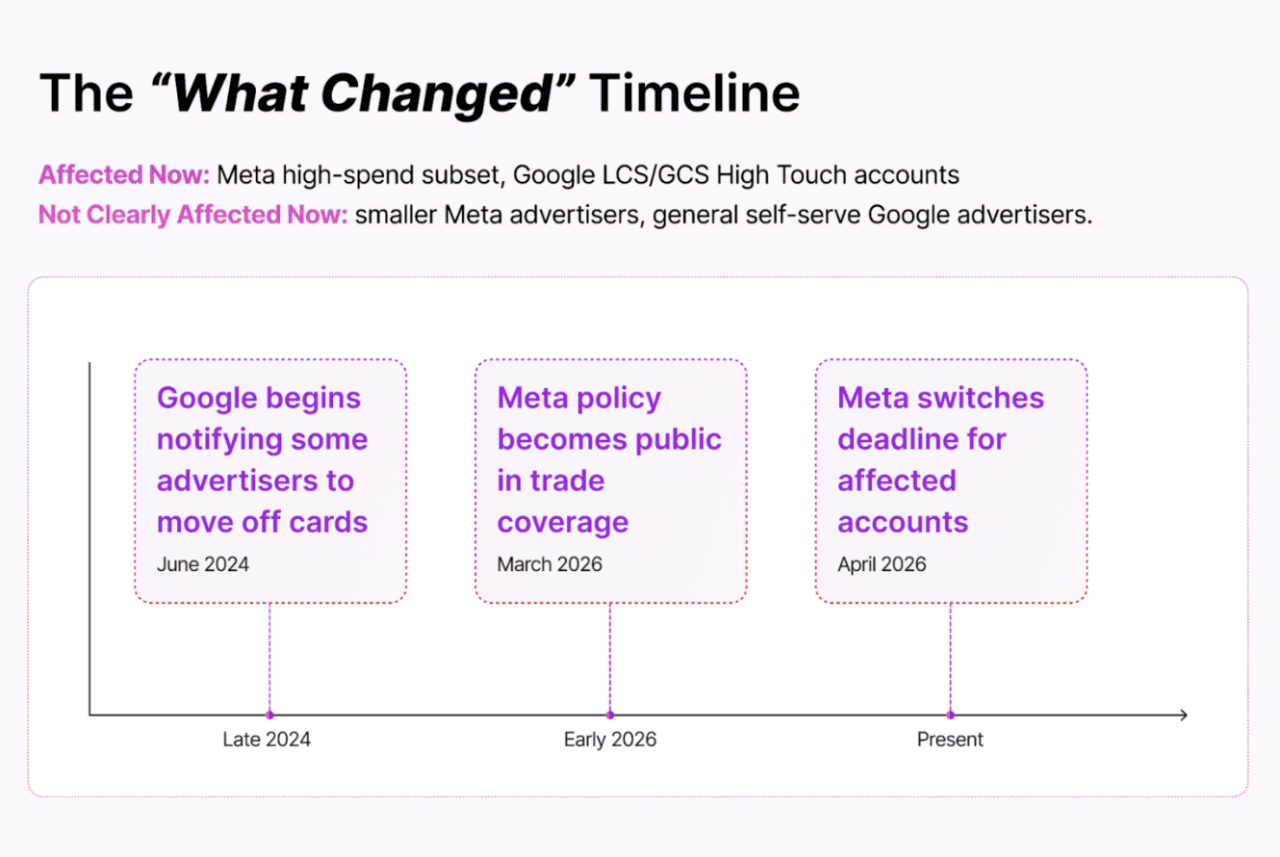

Meta has begun requiring a subset of its advertisers to stop using credit cards to pay for ad spend, pushing them instead toward bank-based billing and monthly invoicing.

For business owners like Brian Waldman, founder of Camp Snap, that shift runs deeper than a billing update. Waldman had structured part of his company’s financial rhythm around the credit card points his Meta ad spend generated, using those rewards to offset real business costs and, when the math worked out well, the occasional trip to the Caribbean.

As this article from elk Marketing examines, losing card access pulls away something many founders had woven into how they actually fund and operate their businesses: a flexible, rewards-generating buffer that sat between their ad spend and their bottom line. This structure is more common than it appears, with many brands relying on credit card billing cycles to bridge the gap between ad spend and incoming revenue.

Waldman’s situation is not an isolated billing adjustment. Meta’s move echoes a policy Google put into motion in 2024, when it began requiring certain high-spend advertisers to abandon card payments entirely in favor of bank-based alternatives.

Credit cards are not disappearing from digital advertising altogether, and smaller advertisers on both platforms remain unaffected for now, but neither platform has disclosed a clear public spend threshold.

But for the businesses spending at scale, the terms of funding growth appear to be changing in ways that could reshape cash flow strategies, eliminate rewards as a legitimate business tool, and shift more of the financial weight of digital advertising directly onto the advertisers themselves.

elk Marketing

What exactly is changing at Meta

On the surface, Meta’s announcement reads like routine billing housekeeping. A spokesperson described the change as “updating and streamlining our billing experience for a very small percentage of advertisers,” adding that the company is “dedicated to making the transition as smooth as possible.”

Smaller advertisers generally appear unaffected for now, but Meta has not disclosed a clear public spend threshold that determines who falls under the requirement. But for those who received the notification, the practical implications run considerably deeper than a procedural update.

Affected advertisers must now fund their ad spend through one of two bank-based alternatives: monthly invoicing, which operates on a 30-day payment cycle tied to an assigned credit line, or direct debit, which pulls payments automatically from a linked bank account.

This does not change how campaigns enter auctions or how ads are optimized. The paid media risk is interruption. If a credit line is reached, payment fails, or billing setup is incomplete, campaigns can pause regardless of how well they are performing.

Meta has not disclosed how many advertisers fall under the new requirement, and the company has declined to reveal the spending thresholds that determine who is affected, leaving a notable gap between its public messaging and the reality facing the businesses now navigating the change.

What Google already did

Meta is not the first platform to redraw the rules on how advertisers pay. Google began notifying certain high-spend advertisers in 2024 that their payment options were changing, giving them until July 31 to complete the transition or risk account suspension.

Ginny Marvin, Google’s Ads Liaison, confirmed the scope at the time, saying that “some customers will move to bank payments via monthly invoicing or direct debit from a bank account.”

Google presented the move as a better fit for larger accounts, telling affected advertisers that monthly invoicing was best suited for their accounts given the flexibility it provides high-growth customers.

Google’s current help documentation also states that advertisers supported by its Large Customer Sales and GCS High Touch teams cannot use credit cards, debit cards, or e-wallets.

Why the platforms are doing this

Several forces are converging to make bank-based billing more attractive to platforms at this scale. The most straightforward is cost.

Every time an advertiser pays by credit card, the merchant, in this case Meta or Google, absorbs a processing fee that typically runs between 1.5% and 3.5% of the transaction. Chris Pollard, founder of Ads Uploader, has watched this math closely. “The savings are enormous,” he told MarketWatch.

Beyond processing costs, bank-based payments and invoicing reduce the billing interruptions card payments often create, from expired cards and spending limits to fraud flags that can pause campaigns mid-flight.

Monthly invoicing also gives both platforms cleaner control over large-account receivables, standardizing approvals and reconciliation in ways that card billing cannot.

Underneath all of it is a basic reality of market position. Gil Luria, an analyst with D.A. Davidson, said Meta is “using every dollar of cash they have,” which helps explain why a platform at this scale would look for structural costs to trim.

How large is the payment opportunity

To appreciate the scale of what both platforms stand to gain, consider the revenue base these payment changes are operating against.

Meta generated $196.2 billion in advertising revenue in 2025, while Alphabet’s Google advertising revenue reached $294.7 billion, putting the combined exposure at roughly $490.9 billion annually.

Neither company has disclosed what share of that revenue currently runs through credit card payment rails, so any figure citing a precise card-paid amount would be speculative. What is defensible is scenario analysis.

Using 2.35% as a rough benchmark for card acceptance costs, shifting just 10% of that combined ad revenue off cards would represent approximately $1.15 billion in potential fee savings. At 25%, that figure climbs to roughly $2.88 billion. At 50%, it approaches $5.77 billion.

Those figures illustrate why even a partial migration of high-spend billing onto cheaper payment rails can matter at this scale.

A Real Margin Lever, With Real Limits

Moving large-advertiser billing off card rails and onto bank-based alternatives could save both platforms hundreds of millions to low billions of dollars in gross payment costs over time, depending on how much spend is actually affected. Those savings would not flow entirely to operating profit, because invoicing and collections carry their own administrative costs, but the direction is margin-positive.

To put the scale in context, Meta reported $83.3 billion in net profit and $115.8 billion in operating cash flow in 2025, while Alphabet generated $129.0 billion in operating income and $164.7 billion in operating cash flow for the same period. A hypothetical $500 million to $1 billion improvement is worth having, but it does not reshape either earnings picture on its own.

For investors, the numbers drawing far more attention are Meta’s rapidly rising expense projections and Alphabet’s planned capital expenditure of $175 billion to $185 billion in the current fiscal year, both of which carry considerably more weight as stock drivers than a change to how ad invoices get paid.

This change is more likely to matter as a signal of cost discipline across the ad stack than as a standalone catalyst, and its full significance still depends on disclosures neither company has yet made.

Who Bears the Cost

Large advertisers and agencies are absorbing the sharpest immediate impact. For high-spend accounts, credit cards served multiple functions beyond simple payment.

They acted as a short-term working capital buffer, a way to centralize spend across multiple brands or client accounts, and a tool for smoothing the timing gap between ad spend going out and customer revenue coming in.

Removing that option adds real operational complexity, requiring bank account setups, invoice approval workflows, and procurement processes that did not previously exist. Agencies that front ad spend on behalf of clients before being reimbursed face particular pressure, since bank-based billing cycles do not always align with client payment schedules.

David Suk, CEO of Baby’s Brew, captured the broader business calculus when he said his company was “looking at other avenues to market” the brand in response to the change. Smaller advertisers are not in the immediate line of fire on either platform, but the direction of travel is worth noting.

SMBs rely disproportionately on cards for liquidity, and if this model expands downstream, smaller businesses would face considerably more financing pressure than enterprises with dedicated treasury teams and established bank credit access.

Impact on credit card points plans and rewards programs

For the advertisers caught in this billing change, the rewards conversation extends well beyond travel perks.

Businesses spending $50,000 or more per month on Meta ads could lose between $12,000 and $18,000 annually in cash back alone, based on a typical 2% to 3% return rate on card spend. Those figures help explain why the reaction has been so immediate.

One advertiser posted on X, “RIP business class flights,” while another calculated their Meta ad rewards at “$400 monthly” in what they described as “free money.”

Dave Grossman, founder of MilesTalk, did not find the frustration surprising. “It’s an obsession,” he said of how seriously business owners approach card rewards accumulation. The broader rewards industry, however, is less likely to feel this at scale.

Card rewards are funded through interchange economics, and without disclosed data on how much total ad spend is actually migrating off cards, the impact on Visa, Mastercard, Amex, or issuing banks remains diffuse. This is a more consequential story for individual advertisers losing a real financial tool than for the rewards market as a whole.

This story was produced by elk Marketing and reviewed and distributed by Stacker.

![]()